Best Debt Consolidation Options UK 2026: Loans, Cards & DMPs Compared

Visual summary of key points from 'Best Debt Consolidation Options UK 2026: Loans, Cards & DMPs Compared'

Essential UK Budgeting & Personal Finance Guides for 2026

Discover practical tips, tools, and strategies to manage your money, save effectively, and stay on top of your finances.

Check out our key articles: How to Create a Simple Budget, How to Save £500 in 3 Months, Understanding Credit Scores in the UK.

Best Debt Consolidation Options in the UK (2026)

If you're juggling multiple debts, consolidation can simplify repayments, reduce interest costs, and help you stay on track. In the UK, there are several reliable options depending on your financial situation, credit score, and whether you own a home. This guide explains each one in plain English — and helps you work out which is right for you.

Important: This article is for informational purposes only and does not constitute financial advice. If you are struggling with debt, consider speaking to a free, regulated debt adviser such as StepChange or National Debtline.

What is debt consolidation?

Debt consolidation means combining multiple debts — such as credit cards, overdrafts, or personal loans — into a single monthly payment. Done correctly, it can reduce the total interest you pay and make your finances easier to manage. Done incorrectly, it can increase your total debt or put your home at risk.

The right option depends on:

- How much you owe and to how many creditors

- Your credit score (which affects the rates available to you)

- Whether you own a home

- How quickly you can realistically repay the debt

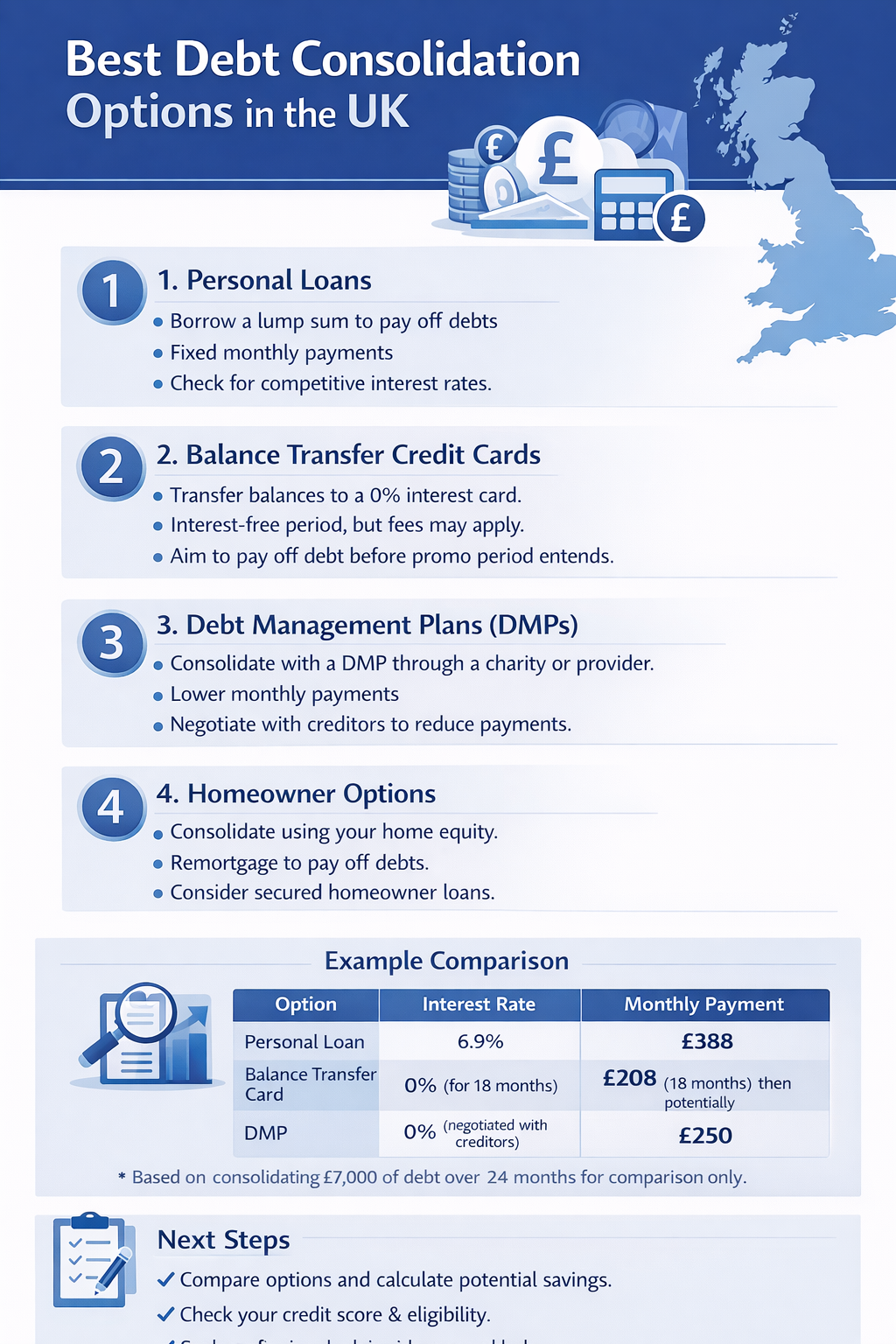

1. Personal loans

A personal loan lets you pay off multiple debts in one go and replace them with a single fixed monthly repayment at a set interest rate. If your credit score is reasonable, this is often the simplest consolidation route.

- Typical UK APR: 6–15% (depending on credit score and loan amount)

- Repayment term: 12–60 months

- Pros: Fixed monthly payments, clear end date, simpler budgeting

- Cons: Good credit usually required; some lenders charge arrangement fees; avoid secured personal loans unless necessary

Compare representative APRs carefully — the rate advertised only has to be offered to 51% of successful applicants. Your actual rate may be higher.

2. Balance transfer credit cards

A 0% balance transfer card lets you move existing credit card debt onto a new card and pay no interest for a promotional period — typically 12 to 30 months. If you can clear the balance within that window, you can save a significant amount in interest.

- 0% interest period: 12–30 months (varies by card and credit score)

- Balance transfer fee: 0–3% of the amount transferred

- Pros: Can save hundreds in interest if repaid within the promotional period

- Cons: High standard APR kicks in after the promo period (typically 18–25%); requires a good credit score; only works for credit card debt, not loans or overdrafts

Set up a direct debit to pay at least the minimum each month — missing a payment can cancel the 0% deal instantly.

3. Debt management plans (DMPs)

A DMP is an informal arrangement where a debt charity negotiates with your creditors on your behalf, consolidating your repayments into one affordable monthly payment. StepChange and National Debtline offer this service free of charge — avoid any company that charges fees for a DMP.

- Monthly payment: Based on what you can genuinely afford after essential living costs

- Interest and charges: Often frozen or reduced by creditors (not guaranteed)

- Pros: Free professional support, single monthly payment, no new borrowing required

- Cons: Will appear on your credit file; not legally binding on creditors; can take several years to clear debt

A DMP is often the right choice if you cannot realistically qualify for a loan or balance transfer card, or if your debt feels unmanageable.

4. Homeowner options (secured loans and remortgaging)

If you own your home, you may be able to consolidate debts by adding them to your mortgage or taking out a secured loan. The lower interest rates can look attractive — but your home is at risk if you miss payments, and you may be paying off the debt over a much longer period, increasing the total interest paid.

- Typical APR: 3–7% (varies significantly by lender and loan-to-value ratio)

- Pros: Lower monthly payments, lower interest rates than unsecured borrowing

- Cons: Your home can be repossessed if you miss payments; spreading short-term debt over a 20-year mortgage can increase total cost significantly

Always get independent financial advice before securing debt against your home. A free session with a debt adviser (StepChange, Citizens Advice) is a sensible first step.

Comparison table

| Option | Typical UK rate | Best if... | Watch out for |

|---|---|---|---|

| Personal loan | 6–15% APR | You have a fair-to-good credit score and want fixed repayments | Arrangement fees; rate offered may differ from advertised |

| Balance transfer card | 0% promo, then 18–25% | You have credit card debt and can repay within the 0% window | Missing a payment cancels the 0% deal; transfer fee of up to 3% |

| Debt management plan | Interest may be frozen | You cannot afford minimum payments and need breathing room | Impact on credit file; not legally binding on creditors |

| Secured loan / remortgage | 3–7% APR | You own your home and have explored all unsecured options first | Home at risk; total interest over a long term may be higher |

How to choose the right option

- Check your credit score first — free tools include Experian, Equifax, and Credit Karma. Your score determines which products you can access and at what rate.

- Calculate the total cost, not just the monthly payment. A lower monthly payment spread over a longer term can cost more overall.

- Never consolidate onto a higher-interest product — if the new rate is higher than your existing debts, it defeats the purpose.

- If you own a home, treat secured borrowing as a last resort rather than a first option.

- If you're unsure, speak to a free debt adviser before making any decision.

Free debt help in the UK

If your debts feel unmanageable, free, regulated support is available:

- StepChange Debt Charity — free debt advice and DMP setup

- National Debtline — free telephone and online advice

- Citizens Advice — local in-person and online support

- MoneyHelper — government-backed financial guidance

Next steps

Start by listing all your debts — amounts owed, interest rates, and minimum payments. Then use our budgeting calculator to understand what you can realistically afford to repay each month. Once you know your budget, the right consolidation option will be much clearer.