How to Improve Your UK Credit Score Quickly (2026): 8 Proven Steps

Visual summary of key points from 'How to Improve Your UK Credit Score Quickly (2026): 8 Proven Steps'

Essential UK Budgeting & Personal Finance Guides for 2026

Discover practical tips, tools, and strategies to manage your money, save effectively, and stay on top of your finances.

Check out our key articles: How to Create a Simple Budget, How to Save £500 in 3 Months, Understanding Credit Scores in the UK.

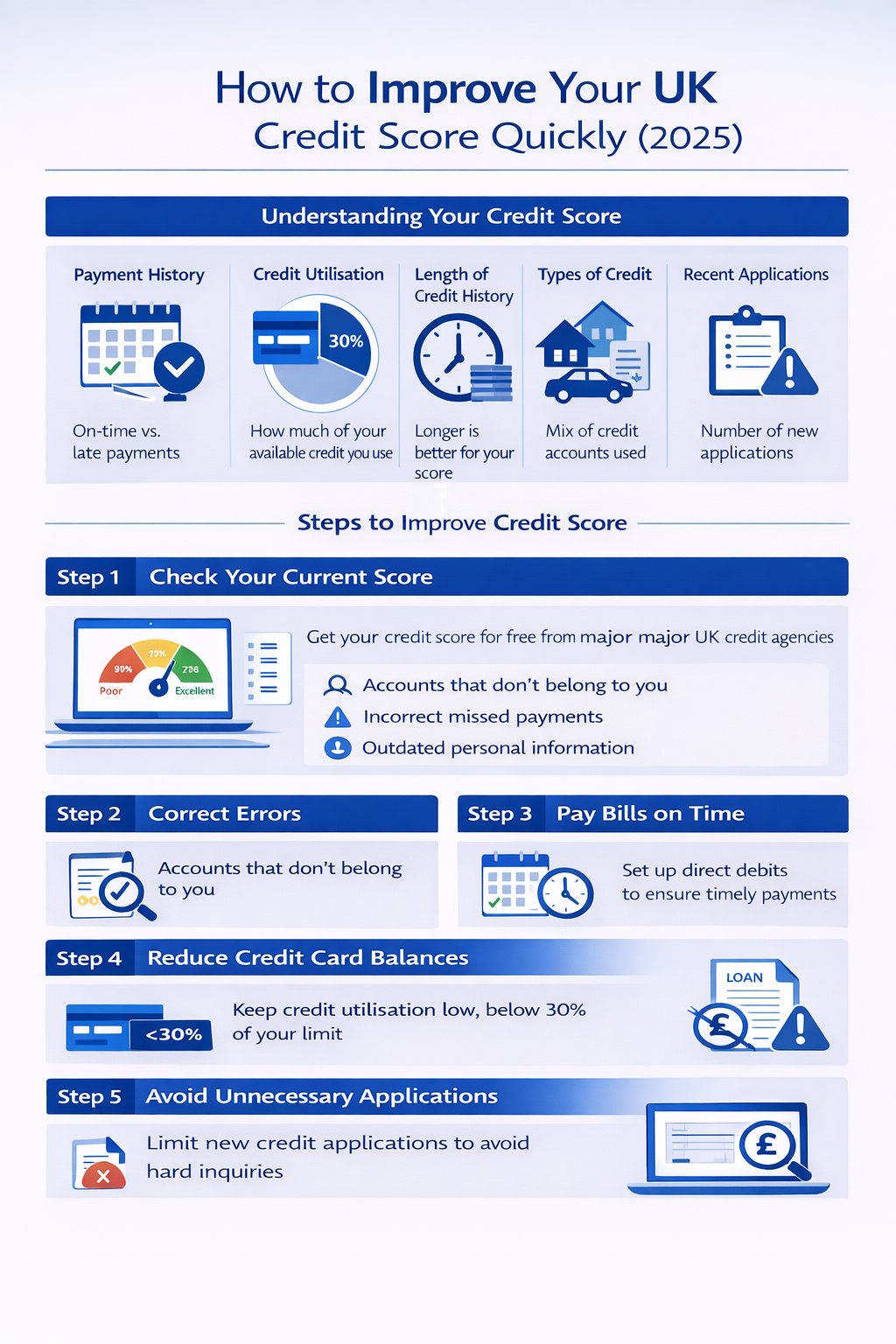

How to Improve Your UK Credit Score Quickly (2026): 8 Proven Steps

Your credit score affects more than just loan applications. In the UK, landlords, mortgage lenders, mobile phone providers, and some employers all check credit histories as part of their decision-making. A poor score does not just mean higher interest rates — it can mean outright rejection for products you need.

The good news is that credit scores are not fixed - and some actions produce results faster than you might expect. Registering on the electoral roll can show an effect within two to four weeks. Reducing your credit utilisation can shift within one to two billing cycles. With consistent action across the eight steps below, meaningful improvement is achievable within three to six months.

Quick-win timeline at a glance

| Action | Typical timeframe to see effect |

|---|---|

| Electoral roll registration | 2–4 weeks |

| Correcting a credit report error | 4–8 weeks (after dispute resolved) |

| Reducing credit utilisation | 1–2 billing cycles (4–8 weeks) |

| Consistent on-time payments | 3–6 months to show meaningful improvement |

| Building thin credit history | 6–12 months for a solid track record |

| Negative marks fading | 2–3 years significantly less impactful; 6 years to drop off |

How UK credit scores work

Unlike the US, the UK does not have a single universal credit score. Three main credit reference agencies operate in the UK — Experian, Equifax, and TransUnion — and each uses a different scoring system and scale:

| Agency | Score range | Good score | Excellent score | Free access |

|---|---|---|---|---|

| Experian | 0–999 | 881–960 | 961–999 | MSE Credit Club, Experian free tier |

| Equifax | 0–1,000 | 531–670 | 811–1,000 | ClearScore (free, powered by Equifax) |

| TransUnion | 0–710 | 566–603 | 628–710 | Credit Karma UK (free) |

Lenders typically check one or two of these agencies — not always all three — which means your score can differ depending on which agency a lender uses. It is worth checking all three periodically, as errors on one may not appear on others.

Step 1 — Register on the electoral roll

This is the fastest single action most people can take. Registering to vote at your current address confirms your identity and address to lenders — both are key factors in credit assessments. If you are not registered, many lenders will decline you automatically regardless of your other credit history.

Register at gov.uk/register-to-vote — it takes five minutes. If you live in shared accommodation or move frequently, update your registration every time you move. The effect on your credit score can appear within a few weeks of registration being confirmed.

Step 2 — Check all three credit reports for errors

Errors on credit reports are more common than most people realise. A 2022 survey found that around one in five UK adults had found an error on their credit file. Common mistakes include:

- Accounts listed as open that you have closed

- Missed payments recorded incorrectly

- Addresses or personal details that are out of date

- Accounts belonging to someone with a similar name (rare but it happens)

- A financial association with an ex-partner still showing on your file

Check your reports for free via ClearScore (Equifax), Credit Karma UK (TransUnion), and MSE Credit Club or Experian's free tier (Experian). Raise a dispute directly with the credit reference agency if you find anything incorrect — they are legally required to investigate within 28 days.

Step 3 — Pay every bill on time, every month

Payment history is the most heavily weighted factor in UK credit scoring. A single missed payment can remain on your credit file for six years and significantly damage your score — particularly if the account goes into default.

The most reliable way to protect your payment history:

- Set up direct debits for every credit card, loan, and bill to cover at least the minimum payment

- Set calendar reminders one week before any manual payments are due

- If you are struggling to make a payment, contact the lender before you miss it — many will arrange a temporary arrangement that does not get recorded as a missed payment

If you have missed payments in the past, the damage diminishes over time. Most negative marks become significantly less impactful after two to three years and drop off entirely after six.

Step 4 — Reduce your credit utilisation below 30%

Credit utilisation is the percentage of your available credit limit that you are currently using. It is one of the fastest-moving factors in your credit score — changes can show up within one to two billing cycles.

| Credit limit | Balance | Utilisation | Impact on score |

|---|---|---|---|

| £5,000 | £4,500 | 90% | Significantly negative |

| £5,000 | £2,000 | 40% | Mildly negative |

| £5,000 | £1,200 | 24% | Positive |

| £5,000 | £250 | 5% | Very positive |

Aim to keep utilisation below 30% across all cards combined, and below 30% on each individual card. If you can get it below 10%, the effect is even more positive. Paying down balances mid-cycle (before your statement date) rather than waiting for the payment due date reduces the utilisation figure that gets reported to credit agencies.

Step 5 — Do not close old credit accounts

Length of credit history is a positive factor — older accounts demonstrate a longer track record of responsible borrowing. Closing a long-standing credit card removes that history from your active score and also reduces your total available credit, which increases your utilisation percentage.

Unless an account has an annual fee you no longer want to pay, the default position should be to keep old accounts open and use them occasionally (even a small purchase once a month) to prevent the lender closing them due to inactivity.

Step 6 — Space out credit applications

Every time you apply for credit — a loan, a credit card, a new phone contract, a mortgage — the lender runs a hard search on your credit file. Hard searches are visible to other lenders for 12 months and each one can temporarily reduce your score by a small amount.

Multiple applications in a short period signal financial stress to lenders, even if each individual application was approved. Space applications at least three months apart where possible. Before applying, use eligibility checkers — offered by most comparison sites and lenders — which use a soft search that does not affect your score.

Step 7 — Build credit history if you have little or none

If you are new to credit in the UK — whether as a young adult, a recent immigrant, or someone who has avoided credit — the challenge is different. You do not have bad credit, you have thin credit, and the solution is building a track record from scratch.

Practical ways to build UK credit history:

- Credit builder credit card — cards like the Aqua Classic, Vanquis, or Capital One Classic are designed for people with thin or poor credit history. They carry high interest rates (typically 30–40% APR) but if you pay the full balance every month you never pay interest and steadily build a positive payment history. Set up a direct debit for the full balance.

- Credit builder loan — products like Loqbox allow you to save a fixed amount monthly and the savings activity is reported to credit agencies as responsible credit behaviour. The "loan" is effectively your own savings returned to you at the end.

- Mobile phone contract — a standard monthly contract (not pay-as-you-go) is a simple form of credit that gets reported and contributes to your history if paid on time.

Step 8 — Remove financial associations with others

If you have ever had a joint bank account, joint mortgage, or joint loan with another person, their credit history is linked to yours — this is called a financial association. If their credit score is poor, it can affect how lenders view your application even if your own history is clean.

If the joint account or product is closed, write to each credit reference agency requesting a notice of disassociation. This removes the link from your file. You cannot do this while a joint account or product is still active.

The timeline table above covers each action in detail. The most important thing is starting - every week of consistent behaviour compounds

Frequently asked questions

- Does checking my own credit score damage it? No. Checking your own score is a soft search and has no impact on your credit file. Only hard searches from lenders affect your score.

- Will paying off a default improve my score immediately? Paying a default marks it as "satisfied" on your file, which looks better than an outstanding default to lenders — but the default itself remains on your file for six years from the original default date regardless of whether it is paid.

- Does my partner's credit score affect mine? Only if you have a financial association (joint account, joint mortgage). Your individual scores are entirely separate unless a product links you financially.

- Can I pay someone to fix my credit score? No legitimate company can remove accurate negative information from your credit file. Any company claiming to do so is engaging in fraud. You can dispute errors yourself for free through each credit reference agency.

- Does income affect credit score? No — income is not recorded on your credit file and does not directly affect your score. However, lenders use income information alongside your credit score in their affordability assessments.