The Ultimate Guide to Budgeting in the UK

Visual summary of key points from 'The Ultimate Guide to Budgeting in the UK | BudgetSense'

Essential UK Budgeting & Personal Finance Guides for 2026

Discover practical tips, tools, and strategies to manage your money, save effectively, and stay on top of your finances.

Check out our key articles: How to Create a Simple Budget, How to Save £500 in 3 Months, Understanding Credit Scores in the UK.

The Ultimate Guide to Budgeting in the UK (2025)

Budgeting doesn’t have to feel restrictive or complicated. In fact, a good budget should do the opposite — it should give you more control, reduce financial stress, and help you enjoy your money with confidence.

With rising living costs across the UK, from higher energy bills to increased grocery prices, managing your money has become more important than ever. Whether you're saving for a house deposit, paying off debt, or simply trying to stop your bank balance disappearing before payday, budgeting provides a clear path forward.

This ultimate guide explains how to build a realistic budget that works in real life. You’ll learn practical techniques used by financial planners and everyday savers across the UK.

By the end of this guide you will know how to:

- Understand exactly where your money goes each month

- Create a sustainable monthly budget

- Build savings automatically

- Reduce unnecessary spending

- Plan for long-term financial goals

Most importantly, you’ll learn how to make budgeting a habit rather than a chore.

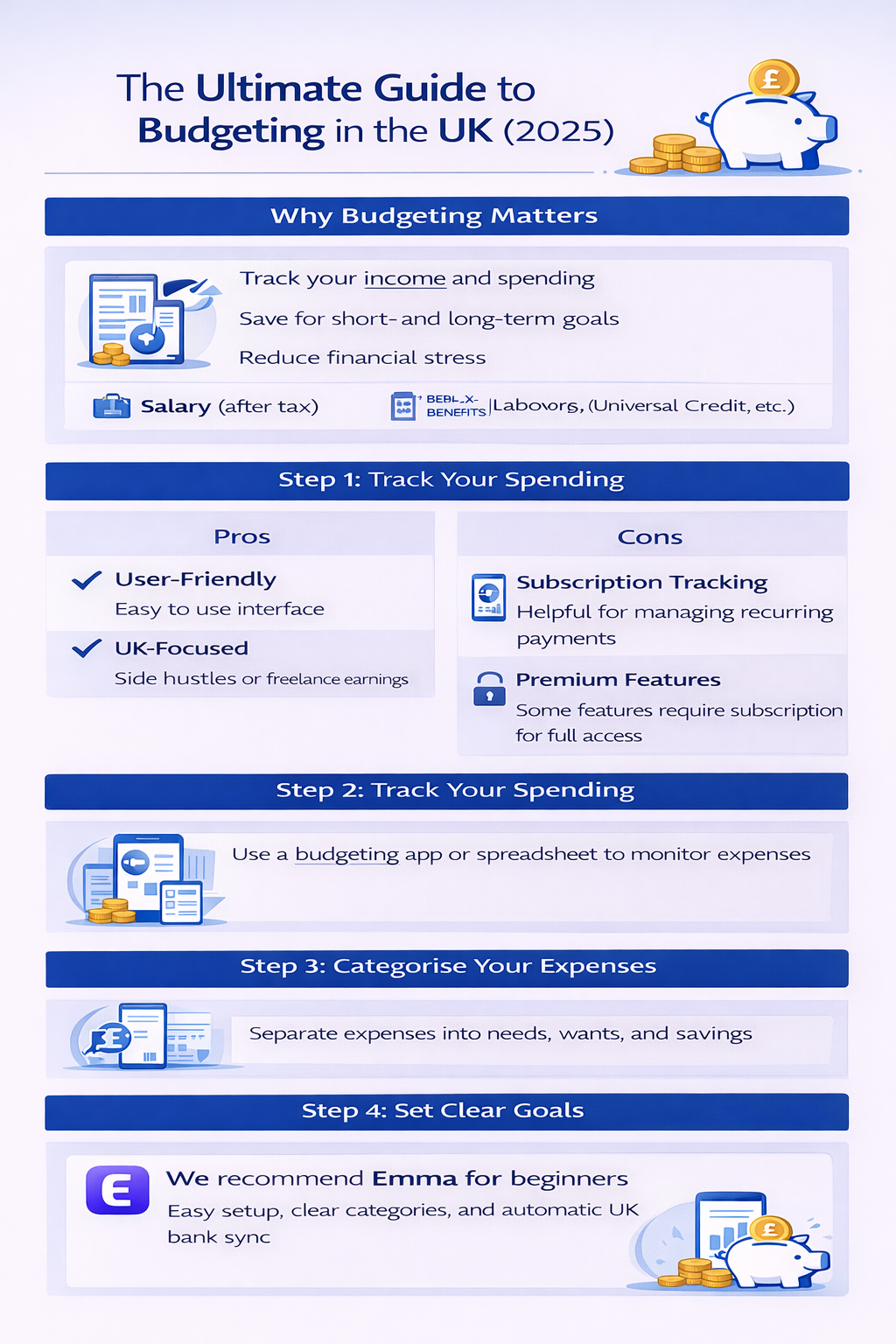

Why Budgeting Matters

A budget is simply a plan for your money. Instead of wondering where your money went at the end of the month, you decide in advance where it should go.

Many people avoid budgeting because they think it means giving up everything they enjoy. In reality, budgeting helps you spend on the things that matter most while cutting back on things that don’t.

A well-structured budget helps you:

- Track your income and spending clearly

- Avoid unnecessary debt

- Build savings faster

- Reduce financial stress

- Prepare for emergencies

- Work toward long-term goals like buying a home or retiring comfortably

Without a budget, it’s very easy for small purchases and subscriptions to slowly drain your finances. Many people underestimate how much they spend on things like takeaway coffee, streaming services, impulse shopping, or food delivery.

When you begin tracking your money, these patterns become visible. Once you see where your money goes, you gain the power to change it.

The Current Cost of Living in the UK

Budgeting has become increasingly important in the UK due to rising costs across many essential areas. Energy bills, rent, groceries, and transport costs have all increased significantly in recent years.

According to UK household data, the average monthly spending for a typical household often includes:

- Housing (rent or mortgage): £800 – £1,500+

- Energy bills: £120 – £300

- Groceries: £250 – £450

- Transport: £100 – £300

- Insurance and subscriptions: £50 – £200

While these numbers vary depending on location and lifestyle, they highlight why having a clear financial plan is essential. Even small changes in spending habits can create hundreds of pounds in savings each year.

Step 1: Understand Your Income

The foundation of any successful budget is knowing exactly how much money you bring in each month.

Start by calculating your total monthly income after tax. This is sometimes called your net income or take-home pay.

Include all reliable sources of income:

- Salary after tax and National Insurance

- Bonuses or commissions (use an average if they vary)

- Government benefits such as Child Benefit or Universal Credit

- Side hustle income

- Freelance or self-employment earnings

- Rental income if applicable

If your income varies from month to month, calculate the average over the past six to twelve months. This provides a realistic baseline for your budget.

It’s generally safer to budget using a slightly conservative income estimate rather than assuming you will always earn the maximum amount.

Step 2: Track Your Spending

The next step is understanding where your money currently goes. Many people are surprised by the results when they start tracking their spending properly.

For at least one full month, record every expense. This includes both large and small purchases.

Typical spending categories include:

- Rent or mortgage payments

- Electricity, gas, and water bills

- Council tax

- Mobile phone and internet

- Transport costs (fuel, public transport, parking)

- Groceries

- Takeaways and restaurants

- Entertainment and hobbies

- Subscriptions (Netflix, Spotify, apps)

- Insurance policies

- Debt repayments

There are several ways to track your spending:

- Bank statements

- Spending tracker apps

- A simple spreadsheet

- Budgeting notebooks

Popular budgeting apps such as Emma or YNAB can automatically categorise spending and connect directly to your bank accounts.

However, many people prefer manual tracking at the beginning because it makes them more aware of each purchase.

Step 3: Categorise Your Expenses

Once you understand your spending, you can group it into categories. This makes it easier to see where adjustments might be possible.

A common budgeting method divides spending into three main areas:

| Category | What it Covers | Suggested % of Income |

|---|---|---|

| Essentials | Rent/mortgage, bills, groceries, transport | 50–60% |

| Lifestyle | Eating out, entertainment, hobbies | 20–30% |

| Savings & Future | Savings, investments, debt repayment | 10–20% |

This approach is sometimes called the 50/30/20 rule. While the exact percentages may vary depending on your situation, the principle remains useful: essential spending should take priority, but there should still be room for enjoyment and future planning.

If your essential expenses are currently higher than 60%, don't panic. Many UK households experience this due to housing costs. The goal is simply to become aware of the situation and gradually improve it where possible.

Step 4: Reduce Unnecessary Spending

Once you can see your spending clearly, opportunities for savings often become obvious.

Common areas where UK households overspend include:

- Unused subscriptions

- Takeaway food

- Impulse online shopping

- Expensive mobile phone contracts

- High insurance renewal prices

Simple strategies to reduce spending include:

- Reviewing subscriptions every three months

- Cooking more meals at home

- Switching energy providers

- Using price comparison websites

- Setting a weekly discretionary spending limit

Even saving £5 per day adds up to over £1,800 per year.

Step 5: Set Clear Financial Goals

Budgeting becomes much easier when you have a clear purpose for your money.

Goals give direction and motivation. Without them, it’s easy to lose focus and fall back into old spending habits.

Financial goals usually fall into three timeframes:

Short-Term Goals (0-12 months)

- Building a £500 emergency fund

- Paying off a credit card

- Saving for a holiday

- Buying a new laptop or phone

Medium-Term Goals (1-5 years)

- Saving for a house deposit

- Starting a business

- Paying off a car loan

- Building a larger emergency fund

Long-Term Goals (5+ years)

- Retirement planning

- Investments and wealth building

- Financial independence

- Funding children’s education

Write down your goals and attach a specific number to them. For example, instead of “save money”, aim for “save £5,000 for a house deposit within two years”.

Step 6: Build an Emergency Fund

An emergency fund is one of the most important elements of financial security.

This is money set aside specifically for unexpected expenses such as:

- Car repairs

- Emergency home repairs

- Medical costs

- Temporary job loss

Financial experts typically recommend saving between three and six months of essential expenses.

However, if that feels overwhelming, start smaller. Even a £500 emergency fund can prevent many financial problems.

Step 7: Automate Your Savings

One of the easiest ways to improve your finances is by automating your savings.

This means setting up automatic transfers from your current account into a savings account each month.

Automation works because it removes the need for constant willpower. The money moves before you have the chance to spend it.

Simple automation strategies include:

- Setting up a standing order the day after payday

- Using separate savings accounts for different goals

- Increasing pension contributions gradually

Many banks now offer features that automatically round up purchases and save the spare change.

Step 8: Use Budgeting Tools

Technology can make budgeting much easier.

Popular budgeting tools in the UK include:

- Emma

- YNAB (You Need A Budget)

- Money Dashboard

- Bank budgeting features within apps

However, the best budgeting tool is the one you will actually use consistently.

Some people prefer digital apps, while others prefer simple spreadsheets or even pen and paper.

Step 9: Review Your Budget Monthly

A budget is not something you create once and forget. It should evolve as your life changes.

Each month, review your finances by asking:

- Did I stay within my planned spending limits?

- Did any unexpected expenses occur?

- Can I increase my savings next month?

- Are any subscriptions no longer needed?

These small monthly adjustments help keep your finances on track.

Common Budgeting Mistakes to Avoid

- Ignoring small purchases that add up over time

- Setting unrealistic spending limits

- Not planning for irregular expenses

- Failing to update your budget regularly

- Giving up after one difficult month

Budgeting is a long-term habit. Progress matters more than perfection.

FAQs

Do I need a strict budget to succeed?

No. A flexible budget is often more effective than a rigid one. The key is consistency rather than strict rules.

Can I budget if I’m self-employed?

Yes. Self-employed workers should budget based on average monthly income and set aside money for taxes.

How much should I save each month?

A common guideline is saving at least 10% of your income. If that feels difficult initially, start smaller and gradually increase it.

Is budgeting worth the effort?

Absolutely. Even basic budgeting can dramatically improve financial stability and reduce stress.

Next Steps

Start today by completing three simple steps:

- Write down your monthly income

- Track your spending for the next 30 days

- Create your first simple budget

Financial progress happens gradually. Small improvements in your spending habits today can lead to significant financial freedom in the future.

The most important thing is to start.