UK Tax Allowances Guide

Visual summary of key points from 'UK Tax Allowances Guide | BudgetSense'

Essential UK Budgeting & Personal Finance Guides for 2026

Discover practical tips, tools, and strategies to manage your money, save effectively, and stay on top of your finances.

Check out our key articles: How to Create a Simple Budget, How to Save £500 in 3 Months, Understanding Credit Scores in the UK.

Ultimate Guide to UK Tax Allowances for Individuals

Understanding UK tax allowances is one of the simplest ways to legally reduce how much tax you pay — yet most people either overlook them or don’t fully use what they’re entitled to. Whether you're employed, self-employed, or managing investments, knowing how these allowances work can make a meaningful difference to your finances.

In this guide, I’ll break down the key UK tax allowances available to individuals, how they work, and practical tax tips UK taxpayers can use straight away. By the end, you’ll have a clear, no-nonsense understanding of how to keep more of your money — without doing anything complicated or risky.

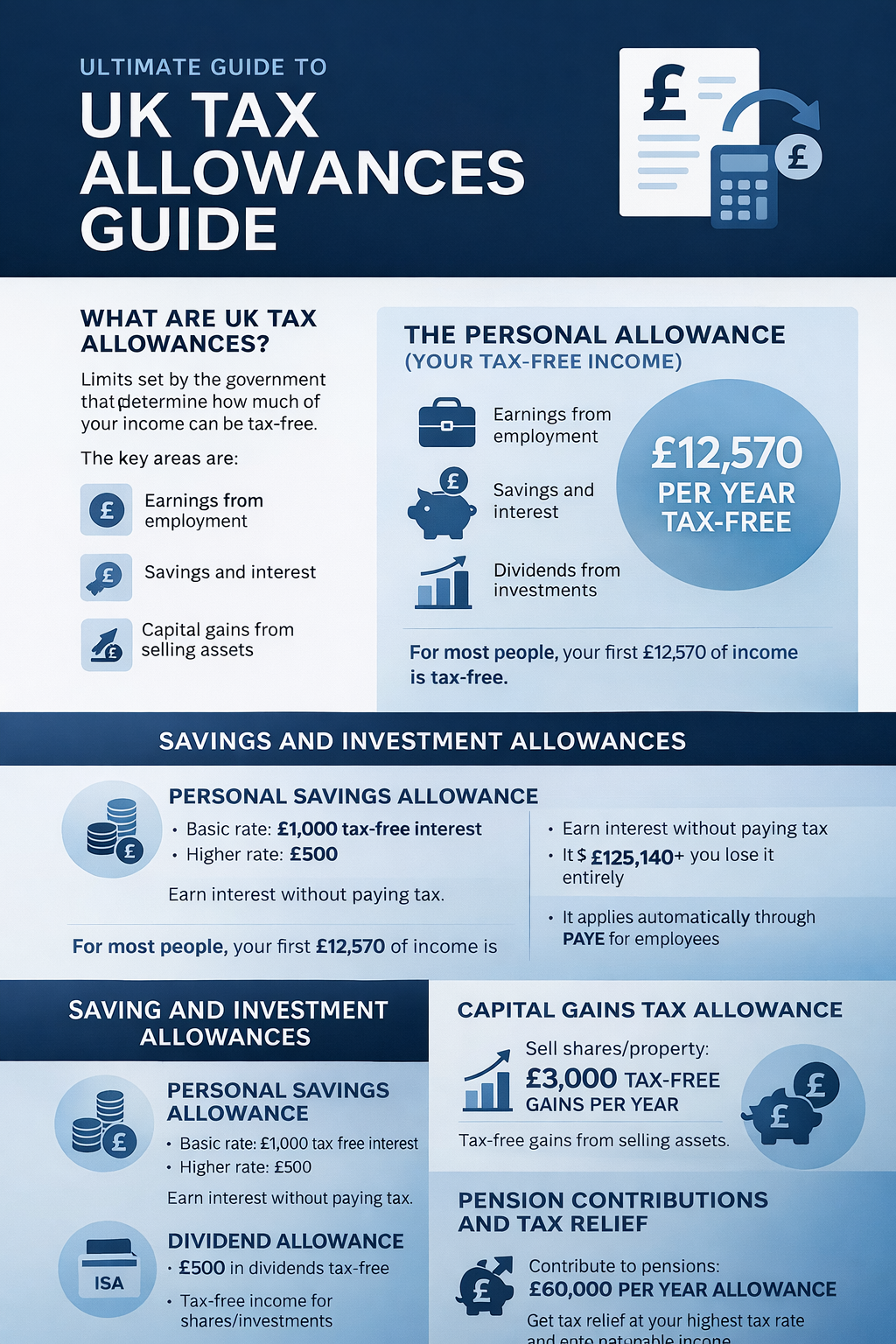

What Are UK Tax Allowances?

At their core, UK tax allowances are limits set by the government that determine how much income you can earn before paying tax — or how much of your income can be tax-free.

These allowances apply across different areas of your finances, including:

- Earnings from employment

- Savings and interest

- Dividends from investments

- Capital gains from selling assets

The key idea is simple: the more allowances you use effectively, the less tax you pay.

For example, if you earn £30,000 a year and your Personal Allowance is £12,570, you only pay income tax on £17,430 — not the full £30,000.

The Personal Allowance (Your Tax-Free Income)

The Personal Allowance is the most important of all UK tax allowances.

For most people, it allows you to earn:

- £12,570 per year tax-free

Anything above this is taxed at the standard income tax rates.

However, there are a couple of key points to be aware of:

- If you earn over £100,000, your Personal Allowance is gradually reduced

- At £125,140+, you lose it entirely

- It applies automatically through PAYE for employees

Marriage Allowance

If you're married or in a civil partnership, you may be able to transfer part of your allowance to your partner.

This can reduce your household tax bill by up to £252 per year.

It’s one of the most underused tax tips UK couples often miss.

Savings and Investment Allowances

Beyond your salary, there are several UK tax allowances that apply to savings and investments — and these are where many people miss opportunities.

Personal Savings Allowance

- Basic rate taxpayers: £1,000 tax-free interest

- Higher rate taxpayers: £500

- Additional rate taxpayers: £0

This is particularly relevant now that interest rates are higher than they’ve been for years.

Dividend Allowance

If you invest in shares, you can receive:

- £500 per year in dividends tax-free

Anything above this is taxed depending on your income band.

ISA Allowance

ISAs are one of the most powerful tools in UK personal finance.

- £20,000 per year tax-free allowance

All interest, dividends, and gains inside an ISA are completely free from tax.

If you’re not using your ISA allowance each year, you’re effectively leaving tax savings on the table. For a deeper breakdown, see our guide on UK Pension Planning Explained.

Capital Gains Tax Allowance

When you sell assets like shares, property (not your main home), or valuable items, you may be liable for Capital Gains Tax (CGT).

However, there is a tax-free allowance:

- £3,000 per year

This means you can make gains up to this amount without paying any tax.

Practical Tip

- Spread disposals across multiple tax years

- Use both partners’ allowances where possible

Pension Contributions and Tax Relief

Pensions are one of the most tax-efficient ways to save in the UK.

When you contribute to a pension:

- You receive tax relief at your highest rate

- Your contributions reduce your taxable income

Annual Allowance

- Up to £60,000 per year

If you’re a higher-rate taxpayer, pension contributions can significantly reduce your overall tax bill and improve long-term financial planning.

Other Useful UK Tax Allowances

There are several lesser-known UK tax allowances that may apply depending on your situation.

Trading Allowance

- £1,000 tax-free side income

Ideal for small side hustles, freelancing, or selling online.

Property Allowance

- £1,000 tax-free property income

Useful if you occasionally rent out a room or space.

How to Make Sure You’re Using All Your Allowances

Knowing about UK tax allowances is one thing — actually using them properly is another.

- Check your tax code regularly

- Use your ISA allowance every year

- Plan before the tax year ends (5th April)

- Track multiple income sources carefully

If you think you’ve overpaid tax, follow our guide on How to Claim UK Tax Refunds Step-by-Step.

Common Mistakes to Avoid

- Not using ISA allowance

- Ignoring dividend tax thresholds

- Missing pension contributions

- Assuming PAYE is always correct

Conclusion

Mastering UK tax allowances isn’t about complicated strategies — it’s about understanding the rules and using them properly.

Use your Personal Allowance, maximise ISAs and pensions, and don’t overlook smaller allowances. Even small changes can lead to meaningful savings over time.

If you want to go further, explore our guides on claiming UK tax refunds and UK pension planning to put these strategies into action.