Best Cheap UK Investment Platforms 2026 — Compared & Ranked

Visual summary of key points from 'Best Cheap UK Investment Platforms 2026 — Compared & Ranked'

Essential UK Budgeting & Personal Finance Guides for 2026

Discover practical tips, tools, and strategies to manage your money, save effectively, and stay on top of your finances.

Check out our key articles: How to Create a Simple Budget, How to Save £500 in 3 Months, Understanding Credit Scores in the UK.

Best Cheap UK Investment Platforms 2026 — Compared & Ranked

Choosing the wrong investment platform could cost you hundreds of pounds a year — sometimes thousands over the long term. With fees eroding returns silently in the background, picking a cheap, trustworthy platform matters just as much as picking what to invest in.

This guide compares the best low-cost UK investment platforms available in 2026, based on platform fees, trading costs, account types, and who each one suits best. All platforms listed are regulated by the Financial Conduct Authority (FCA).

Important: Capital is at risk. The value of investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice.

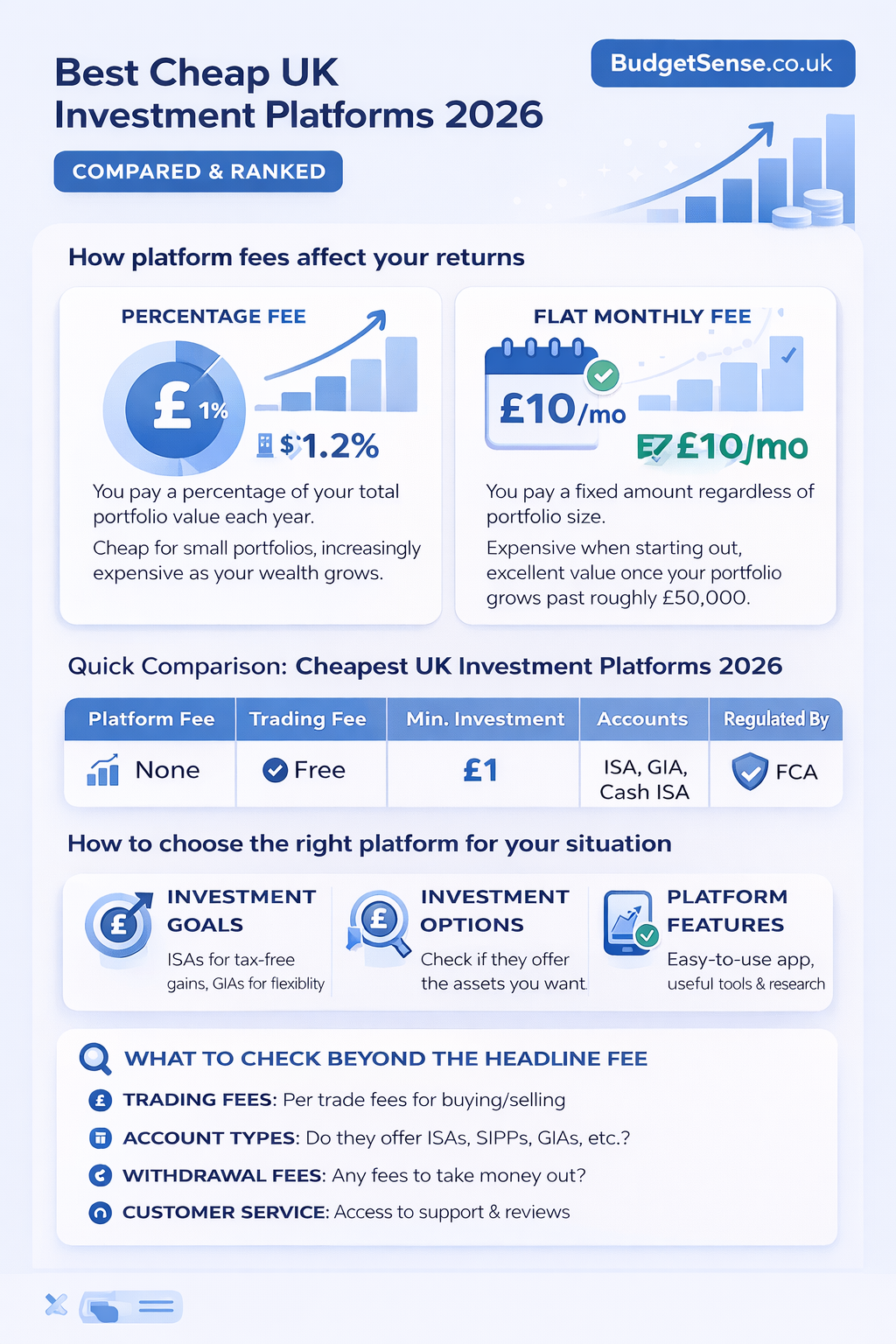

How platform fees affect your returns

Platform fees are the single biggest variable you control as an investor. To illustrate: if you invested £50,000 in funds growing at 10% a year, your portfolio would be worth around £336,000 after 20 years on a zero-fee platform. Choose a platform charging 0.45% annually and you would end up with almost £30,000 less — purely from fees compounding against you.

There are two main fee structures:

- Percentage fee: You pay a percentage of your total portfolio value each year. Cheap for small portfolios, increasingly expensive as your wealth grows.

- Flat monthly fee: You pay a fixed amount regardless of portfolio size. Expensive when starting out, excellent value once your portfolio grows past roughly £50,000.

Quick comparison: cheapest UK investment platforms 2026

Fees correct as of March 2026. Always verify on the platform's own website before opening an account.

| Platform | Platform fee | Trading fee | Account types | Best for |

|---|---|---|---|---|

| Trading 212 | None | Free | ISA, GIA, Cash ISA | Complete beginners, £1 minimum |

| InvestEngine | None | Free (ETFs only) | ISA, GIA, SIPP | Passive ETF investors |

| Freetrade | £60/year (Standard) | Free | ISA, GIA, SIPP | Cost-conscious active investors |

| Vanguard | 0.15% (max £375/yr) | Free | ISA, GIA, SIPP, JISA | Long-term index fund investors |

| AJ Bell | 0.25% on funds (shares capped) | £5 (free on regular plans) | ISA, GIA, SIPP, LISA, JISA | Wide asset range, research tools |

| Interactive Investor | £4.99–£19.99/month flat | Included on some plans | ISA, GIA, SIPP, JISA | Larger portfolios (£50,000+) |

| XTB | None | Free (up to €100k/month) | GIA only | Active traders, no ISA needed |

How to choose the right platform for your situation

Portfolio under £20,000 — go free or percentage-fee

At this level, flat-fee platforms like Interactive Investor (from £4.99/month) often cost more than the portfolio earns. Stick to free platforms like Trading 212 or InvestEngine, or low-percentage options like Vanguard (0.15%) which stay cheap while your portfolio is small.

Portfolio over £50,000 — consider a flat monthly fee

Once your portfolio grows, a flat fee becomes dramatically cheaper than a percentage. Interactive Investor's £11.99/month Investor plan works out to just 0.03% annually on a £500,000 portfolio — far cheaper than platforms still charging 0.25–0.45%.

Investing passively in index funds or ETFs

If you plan to invest monthly into a handful of index funds and not trade actively, you almost never need to pay trading fees. Trading 212, InvestEngine, and Vanguard all offer free regular investing with no per-trade charges.

Platform reviews

1. Trading 212 — best for beginners

Trading 212 is the cheapest all-round option for most UK beginners in 2026. There are no platform fees, no trading fees on shares or ETFs, and you can start with as little as £1. It offers a Stocks & Shares ISA, a Cash ISA, and a general investment account.

The ISA is flexible — you can withdraw and replace money in the same tax year without affecting your £20,000 allowance. Trading 212 also pays competitive interest on uninvested cash.

- Platform fee: None

- Trading fee: Free

- Minimum investment: £1

- Accounts: ISA, GIA, Cash ISA

- Regulated by: FCA

Note: Trading 212 also offers CFDs (contracts for difference), which are high-risk products. Stick to the Invest or ISA section and ignore the CFD section entirely as a long-term investor.

2. InvestEngine — best for ETF investors

InvestEngine specialises in ETFs and is completely fee-free — no platform charges, no trading costs. It is a Which? Recommended Provider and Great Value badge winner for 2026. You can open a Stocks & Shares ISA, a SIPP (pension), or a general account.

The limitation: InvestEngine only offers ETFs. If you want to invest in individual company shares or actively managed funds, you will need a different platform.

- Platform fee: None

- Trading fee: Free

- Minimum investment: £100 to open, then any amount

- Accounts: ISA, GIA, SIPP

- Regulated by: FCA

3. Freetrade — best for shares on a budget

Freetrade offers commission-free trading across around 6,000 UK, European, and US shares plus ETFs. The Standard plan costs £60/year and includes a Stocks & Shares ISA. The Plus plan (£120/year) adds a SIPP and better interest rates on uninvested cash. Freetrade is now part of IG Group and holds a Which? Great Value badge for 2026.

- Platform fee: £60/year Standard (includes ISA), £120/year Plus

- Trading fee: Free

- Minimum investment: £2

- Accounts: ISA, GIA, SIPP (Plus plan)

- Regulated by: FCA

4. Vanguard — best for long-term index fund investors

Vanguard charges 0.15% annually, capped at £375/year — making it one of the cheapest percentage-fee options available. It offers its own range of low-cost index funds and ETFs, widely considered among the best passive investment products available to UK investors.

Vanguard is best for investors who want to set up a regular contribution into a simple index fund and leave it alone for 10–20 years. The range is intentionally limited — which is a feature, not a problem, for most long-term savers.

- Platform fee: 0.15% per year (max £375)

- Trading fee: Free

- Minimum investment: £500 lump sum or £100/month

- Accounts: ISA, GIA, SIPP, Junior ISA

- Regulated by: FCA

5. AJ Bell — best for range and research

AJ Bell is a Which? Recommended Provider for 2026 with nearly 9,000 assets available — the widest range of any platform in this review. It charges 0.25% on funds (shares are capped at a lower percentage rate) and £5 per trade, though trades are free when set up as a regular monthly investment.

- Platform fee: 0.25% on funds (shares capped)

- Trading fee: £5 per trade (free on regular monthly investments)

- Minimum investment: £500 lump sum or £25/month

- Accounts: ISA, GIA, SIPP, LISA, Junior ISA

- Regulated by: FCA

6. Interactive Investor — best for larger portfolios

Interactive Investor charges a flat monthly fee rather than a percentage, which makes it expensive for small portfolios but excellent value as your wealth grows. The Investor Essentials plan (for portfolios up to £50,000) costs £4.99/month. The Investor plan is £11.99/month and includes a Junior ISA.

With over 40,000 investments across 17 international markets, ii is the platform of choice for experienced DIY investors managing significant portfolios.

- Platform fee: £4.99–£19.99/month flat

- Trading fee: Included on some plans; free monthly trades on others

- Minimum investment: None

- Accounts: ISA, GIA, SIPP, Junior ISA

- Regulated by: FCA

7. XTB — best zero-fee option without an ISA

XTB offers zero platform fees and commission-free trading up to €100,000 per month. It is a strong option if you do not need the tax wrapper of an ISA. Note: XTB does not currently offer a Stocks & Shares ISA or SIPP, meaning all gains are subject to capital gains and dividend tax above your annual allowances.

- Platform fee: None

- Trading fee: Free (up to €100k/month)

- Minimum investment: None

- Accounts: GIA only (no ISA or SIPP)

- Regulated by: FCA

What to check beyond the headline fee

Platform fees are only part of the true cost of investing. Always check:

- Fund charges (OCF/TER): Charged by the fund manager, not the platform. Typically 0.05–0.25% for index funds, up to 1.5% for active funds.

- Foreign exchange fees: Charged when buying overseas shares — typically 0.15–1.5%. This adds up quickly for US stock investors.

- Exit fees: Some platforms charge £25–£100+ per fund to transfer away. Check before committing.

- Inactivity fees: XTB and IG charge fees if you do not trade for an extended period.

- Interest on uninvested cash: Some platforms pay nothing; others (Trading 212, Freetrade Plus) pay competitive rates.

Don't forget your ISA allowance

Every UK adult has a £20,000 annual ISA allowance for the 2025/26 tax year (ending 5 April 2026). Investing inside a Stocks & Shares ISA means you pay no income tax on dividends and no capital gains tax on profits — ever. For most investors, using a Stocks & Shares ISA should be the first priority before a general investment account.

For more on ISA options, see our guide to best ISAs for UK savers in 2026.

Next steps

Start by deciding how much you plan to invest and how often. If you are new to investing, our investing for beginners UK guide walks you through the basics before you open an account. If you already know what you want, use our budgeting calculator to work out how much you can realistically set aside each month.

Sources: Which? Investment Platform Review (January 2026), UK StockBrokers.com, Investing Insiders, MoneySavingExpert. Fees verified March 2026. This article may contain affiliate links — if you click and open an account, we may earn a small commission at no extra cost to you.