50 Easy Ways to Save £100 a Month in the UK (2026 Guide)

Visual summary of key points from '50 Easy Ways to Save £100 a Month in the UK (2026 Guide)'

Essential UK Budgeting & Personal Finance Guides for 2026

Discover practical tips, tools, and strategies to manage your money, save effectively, and stay on top of your finances.

Check out our key articles: How to Create a Simple Budget, How to Save £500 in 3 Months, Understanding Credit Scores in the UK.

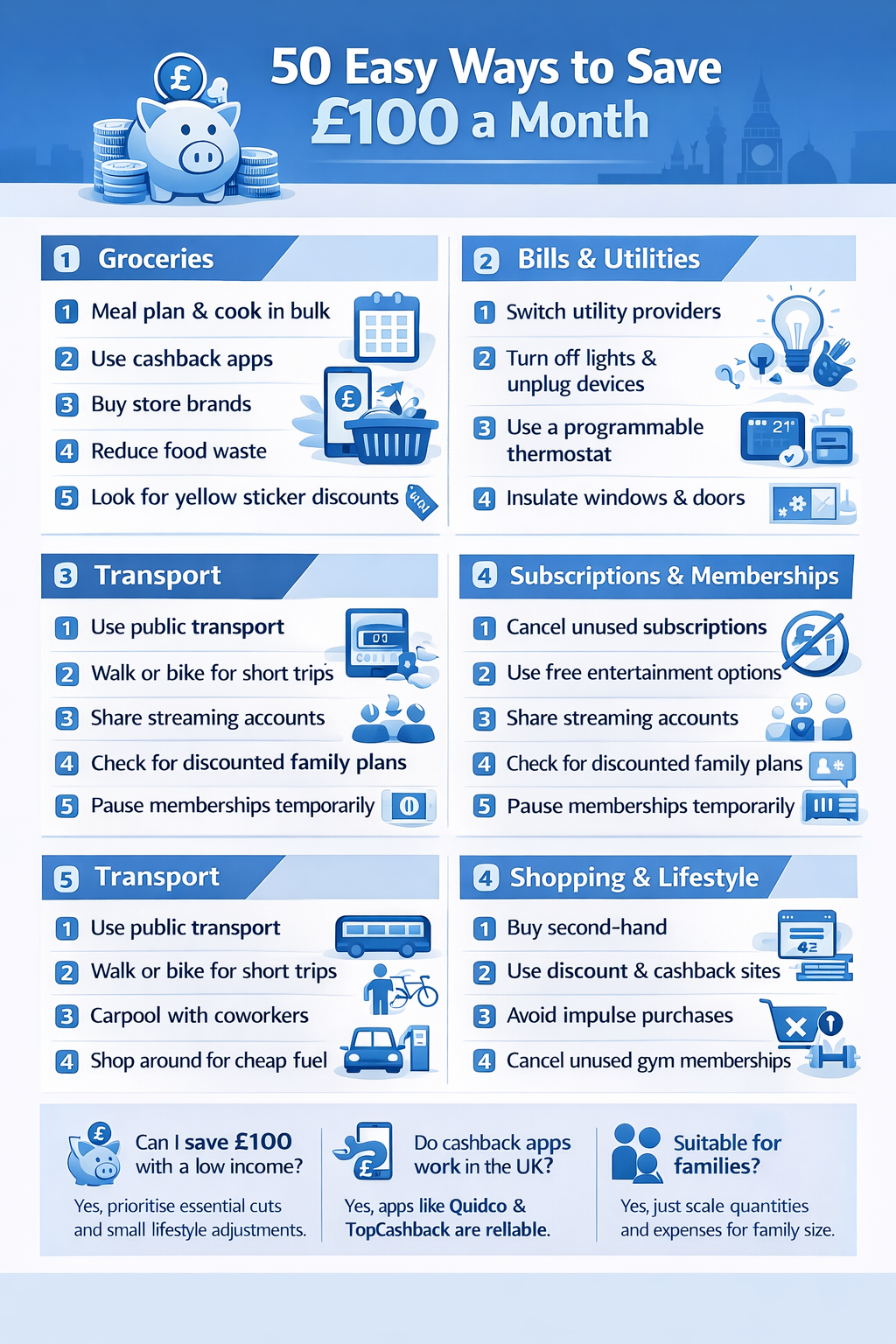

50 Easy Ways to Save £100 a Month in the UK (2026)

Saving £100 a month might sound like a stretch — but for most UK households, it's achievable without any dramatic lifestyle changes. The key is combining several small wins rather than looking for one big fix. Cut £20 from your food shop, £15 from subscriptions, £20 from transport, and £15 from impulse spending and you're already there.

This guide gives you 50 practical, UK-specific ideas across five categories. You don't need to do all 50 — pick the ones that fit your life and build from there. Done consistently, £100 a month becomes £1,200 a year.

Groceries (tips 1–10)

Food is one of the easiest areas to cut without feeling deprived. Planning and awareness make the biggest difference — not deprivation.

| # | Action | Estimated monthly saving |

|---|---|---|

| 1 | Switch to own-brand products for staples (pasta, rice, tins, dairy) | £20–£40 |

| 2 | Plan weekly meals before you shop — reduces waste and impulse buys | £10–£20 |

| 3 | Buy in bulk for non-perishables you use regularly | £5–£15 |

| 4 | Use Clubcard, Nectar, or Asda Rewards — but only on items you'd buy anyway | £5–£10 |

| 5 | Compare prices using Trolley.co.uk before your weekly shop | £5–£10 |

| 6 | Cut takeaways from weekly to fortnightly | £15–£30 |

| 7 | Freeze leftovers immediately rather than letting them go to waste | £5–£10 |

| 8 | Buy seasonal produce — cheaper, fresher, and often better quality | £5–£15 |

| 9 | Add 2–3 meat-free meals per week using eggs, lentils, or beans | £10–£20 |

| 10 | Shop at the end of the day for yellow-sticker reductions | £5–£15 |

Bills & utilities (tips 11–20)

Switching and negotiating takes an hour but can save more than almost anything else on this list. Most people never do it — which is why providers keep raising prices quietly.

| # | Action | Estimated monthly saving |

|---|---|---|

| 11 | Compare energy tariffs on Ofgem-approved sites and switch if cheaper | £15–£30 |

| 12 | Replace old bulbs with LED — uses around 80% less energy | £5–£10 |

| 13 | Turn off devices fully rather than leaving on standby | £5–£10 |

| 14 | Turn heating down by 1°C — saves roughly 10% on heating bills | £10–£20 |

| 15 | Check if a water meter would save you money (good for small households) | £5–£15 |

| 16 | Negotiate broadband renewal — threatening to leave usually gets a better deal | £10–£20 |

| 17 | Bundle broadband, TV, and mobile with one provider for a discount | £5–£15 |

| 18 | Use a smart thermostat (e.g. Hive, Tado) to heat only when needed | £5–£15 |

| 19 | Check if you're owed a council tax discount — single occupancy is 25% off | £5–£25 |

| 20 | Switch home and car insurance at renewal rather than auto-renewing | £10–£30 |

Subscriptions & memberships (tips 21–30)

The average UK household now spends over £50 a month on subscriptions — much of it on services rarely used. A 20-minute audit is one of the fastest ways to free up cash.

| # | Action | Estimated monthly saving |

|---|---|---|

| 21 | Cancel streaming services you haven't used in the last month | £5–£15 |

| 22 | Rotate streaming subscriptions — subscribe to one, watch it, cancel, switch | £5–£15 |

| 23 | Cancel unused gym membership and switch to free outdoor workouts or YouTube | £10–£30 |

| 24 | Audit app subscriptions on your phone (Settings → Subscriptions on iPhone) | £5–£15 |

| 25 | Cancel magazine and newspaper subscriptions you read inconsistently | £5–£10 |

| 26 | Use free tiers of apps (Spotify free, Duolingo free) instead of paid | £5–£10 |

| 27 | Check for student, NHS, or Blue Light Card discounts on remaining subscriptions | £5–£10 |

| 28 | Cancel unused club memberships or annual passes | £5–£20 |

| 29 | Use free online learning platforms (Coursera audit, Khan Academy, YouTube) | £5–£15 |

| 30 | Review software subscriptions — free alternatives often exist (LibreOffice, GIMP) | £5–£15 |

Transport (tips 31–40)

Transport is often the second biggest household expense after housing. Small habit changes here add up faster than in most other categories.

| # | Action | Estimated monthly saving |

|---|---|---|

| 31 | Use public transport for commutes where cost is lower than fuel plus parking | £10–£30 |

| 32 | Walk or cycle short distances under 2 miles instead of driving | £5–£15 |

| 33 | Carpool with colleagues — split fuel costs for shared commutes | £10–£25 |

| 34 | Use PetrolPrices.com to find the cheapest fuel near you | £5–£15 |

| 35 | Keep tyres at correct pressure — reduces fuel consumption by up to 3% | £5–£10 |

| 36 | Buy a railcard if you travel by train regularly (16-25, Two Together, Senior) | £10–£25 |

| 37 | Book train tickets in advance using Trainline or directly with operators | £5–£20 |

| 38 | Use contactless daily/weekly caps on TfL rather than buying tickets | £5–£10 |

| 39 | Switch to cheaper car insurance at renewal — don't auto-renew | £10–£30 |

| 40 | Combine errands into one trip to reduce fuel use and mileage | £5–£10 |

Shopping & lifestyle (tips 41–50)

Lifestyle spending is the easiest area to trim without feeling like you're cutting back — small friction points and habit changes make a big difference.

| # | Action | Estimated monthly saving |

|---|---|---|

| 41 | Buy second-hand clothes on Vinted, eBay, or Facebook Marketplace | £10–£25 |

| 42 | Use TopCashback or Quidco for online purchases you're making anyway | £5–£15 |

| 43 | Wait 48 hours before non-essential purchases — reduces impulse buying significantly | £10–£20 |

| 44 | Repair household items before replacing — YouTube has guides for almost everything | £5–£20 |

| 45 | Switch to a reusable coffee cup and make coffee at home most days | £10–£20 |

| 46 | Reduce alcohol bought outside the home — pub and restaurant margins are very high | £10–£25 |

| 47 | Use price comparison tools (Google Shopping, PriceRunner) before buying anything over £20 | £5–£15 |

| 48 | Set a firm monthly limit for non-essential spending and track it with a budgeting app | £10–£20 |

| 49 | DIY small home and garden jobs rather than hiring — painting, flat-pack, basic plumbing | £5–£25 |

| 50 | Use loyalty points and reward schemes before they expire | £5–£10 |

How to make this work in practice

The most common reason people don't save consistently isn't lack of willpower — it's lack of a system. A few principles that help:

- Automate first. Set up a standing order to move money into savings the day you get paid, before you can spend it. Even £50 a month builds to £600 a year without you noticing.

- Pick your top five. Choose the five tips from this list most relevant to your spending and focus on those first. Trying to implement all 50 at once leads to none of them sticking.

- Review monthly. Spending patterns change. A quick 10-minute review of your bank statement each month shows where the leaks are.

- Track progress. Use a budgeting app or a simple spreadsheet. Seeing your savings grow is one of the strongest motivators to keep going.

For more on building a consistent savings habit, see our guide on how to save money consistently on a UK budget. For a structured approach to managing everything, our ultimate guide to budgeting in the UK walks through the full process.

Frequently asked questions

- Can I save £100 a month on a low income? Yes — in fact, some of the biggest wins (switching energy, cancelling unused subscriptions, reducing takeaways) are equally available regardless of income. Focus on the high-impact, low-effort changes first.

- Do cashback apps actually pay out in the UK? Yes. TopCashback and Quidco are both well-established and have paid out hundreds of millions of pounds to UK users. The key is to always start your purchase from the cashback site or app.

- Should I track every single penny? No — detailed tracking works for some people but burns others out. Focus on the three or four categories where you spend the most and monitor those.

- Are these tips realistic for families? Yes. Many tips — especially around groceries, subscriptions, and transport — scale well for households of any size. Buying in bulk and meal planning tend to have even bigger returns for larger families.

- How long before I notice a difference? If you implement five or more of these changes, you should see a measurable difference within the first full month. The compounding effect becomes more visible after three to six months.