How to Save Money Consistently in the UK (2026): A Practical Guide

Visual summary of key points from 'How to Save Money Consistently in the UK (2026): A Practical Guide'

Essential UK Budgeting & Personal Finance Guides for 2026

Discover practical tips, tools, and strategies to manage your money, save effectively, and stay on top of your finances.

Check out our key articles: How to Create a Simple Budget, How to Save £500 in 3 Months, Understanding Credit Scores in the UK.

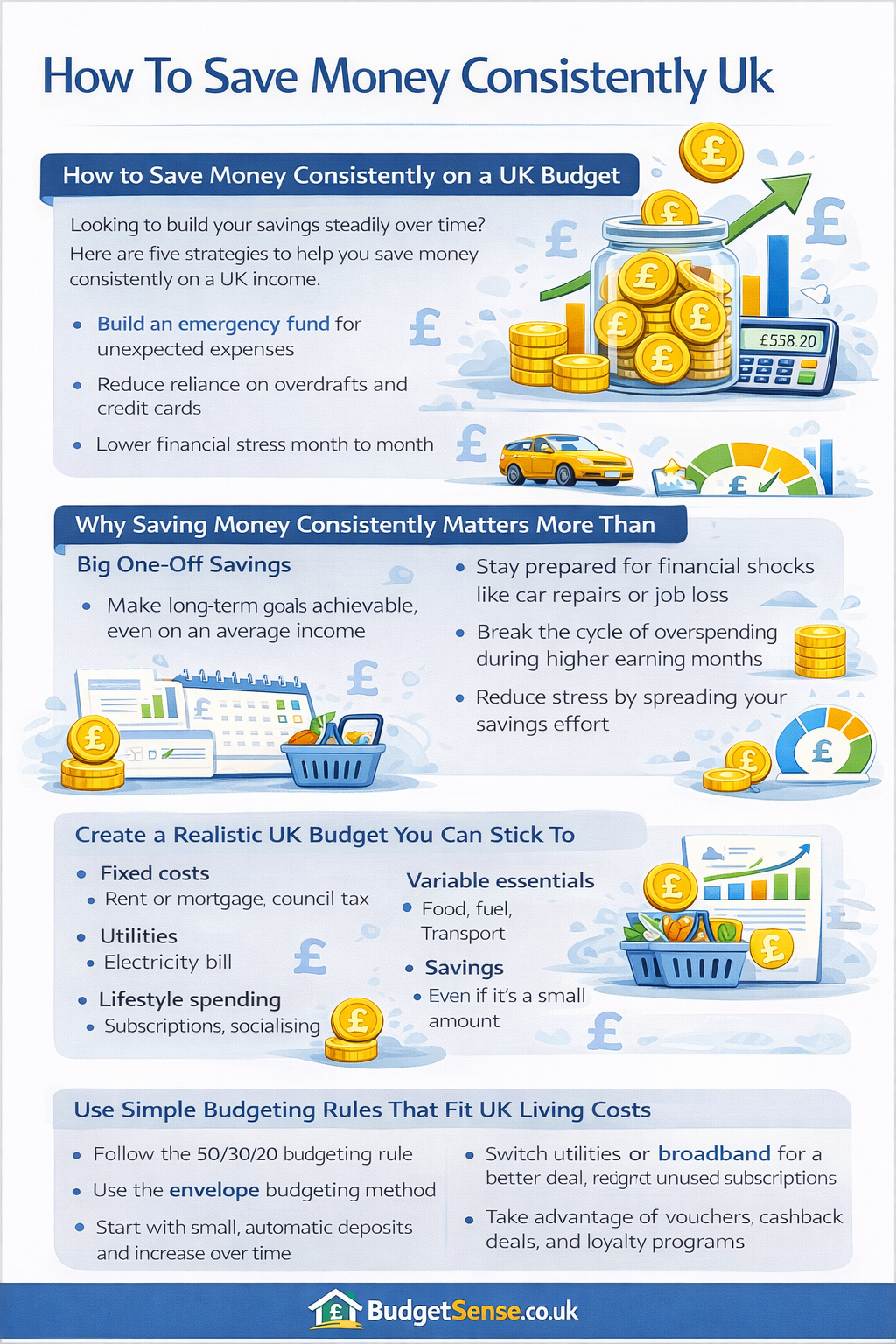

How to Save Money Consistently on a UK Budget (2026)

Saving consistently is less about how much money you earn and more about the system you build around it. Most people who struggle to save aren't undisciplined — they just don't have a structure that makes saving happen automatically. Once that structure is in place, saving stops feeling like a monthly battle and starts feeling unremarkable.

This guide covers the practical steps to build that structure on a UK budget in 2026 — from setting up automation to handling the irregular expenses that derail most savings plans.

Why consistency matters more than amount

A common misconception is that saving only counts when you're putting away large sums. In reality, consistency compounds far more powerfully than occasional large deposits.

Saving £20 a week adds up to £1,040 in a year. Saving £50 a month reaches £600. Neither requires a pay rise or dramatic lifestyle change — just a repeatable habit. The psychological benefit is equally significant: consistent saving builds financial confidence and reduces the low-level stress that comes from having nothing set aside.

The goal is not to find a perfect amount to save. The goal is to make saving so automatic that you stop noticing it.

Step 1 — Build a budget that reflects real life

If your budget only works on a good month, it isn't a useful budget. A realistic UK budget accounts for the messy reality of irregular income, fluctuating bills, and genuine lifestyle costs — not an idealised version of your spending.

Start with four categories:

- Fixed essentials — rent or mortgage, council tax, utilities, insurance, minimum debt repayments

- Variable essentials — food, fuel, transport, prescriptions

- Lifestyle spending — subscriptions, socialising, eating out, hobbies

- Savings — even a small fixed amount, treated as non-negotiable

The savings category goes in before lifestyle spending — not after. If you wait to see what's left at the end of the month, there is rarely anything left. Pay yourself first, then spend what remains.

If you're not sure where your money is currently going, spend one month tracking it before building your budget. Our guide to 5 simple ways to track your expenses covers the quickest methods without turning it into a full-time job.

Step 2 — Automate your savings on payday

Automation is the single most effective change most people can make. By setting up a standing order to move money into a savings account on the day you get paid, you remove willpower from the equation entirely. The money leaves before you can spend it.

Practical ways to automate savings in the UK:

- Standing order to a separate savings account — set it to leave on payday. Even £25 or £50 a month is a start.

- Round-up features — apps like Monzo, Starling, and Chase UK round up transactions to the nearest pound and sweep the difference into savings automatically.

- Savings pots — most UK challenger banks let you create named pots (Emergency Fund, Holiday, Car MOT) within your account so money stays organised without needing multiple bank accounts.

- Employer pension contributions — if your employer matches contributions above the minimum, increasing your pension contribution is effectively free money saved automatically before tax.

For a comparison of apps that make automation easy, see our guide to the best UK budgeting apps reviewed.

Step 3 — Use a budgeting framework that fits UK costs

The 50/30/20 rule — 50% on needs, 30% on wants, 20% on savings — is a useful starting point, but it needs adapting for UK reality. Housing costs alone often exceed 35–40% of take-home pay in many parts of England, leaving less room for the textbook ratios.

A more flexible approach:

| Category | Ideal target | Minimum to aim for |

|---|---|---|

| Essentials (housing, bills, food) | 50% | Up to 60% if housing costs are high |

| Lifestyle and wants | 30% | 20–25% — reduce here before cutting savings |

| Savings and debt repayment | 20% | 5–10% minimum — protect this first |

The exact percentages matter less than the principle: savings come out first, lifestyle spending adjusts to whatever is left. Saving 5% consistently for a year produces better results than saving 20% for two months and then giving up.

Step 4 — Cut spending you don't value, not spending you enjoy

Sustainable saving does not mean eliminating everything enjoyable. It means redirecting money from things you're paying for but not actually valuing.

The most common money leaks in UK households:

- Subscriptions that auto-renewed and are rarely used — audit these via your bank statement or iPhone/Android subscription settings

- Insurance policies that weren't switched at renewal — loyalty penalties are substantial; switching annually typically saves £50–£200 per policy

- Mobile and broadband contracts that rolled past their minimum term — you are usually on a higher tariff once out of contract

- Energy tariffs not reviewed since prices changed — use Ofgem-approved comparison sites to check

- Bank accounts paying no interest on savings — moving to a high-interest easy-access account takes 15 minutes and costs nothing

The discipline here is redirecting any freed-up money directly into savings rather than absorbing it back into general spending. Transfer it on the same day you make the saving.

Step 5 — Use sinking funds for predictable irregular expenses

One of the most common reasons savings plans fail is unexpected expenses wiping them out — except most of these expenses aren't actually unexpected. Car MOTs, Christmas, annual insurance renewals, school uniforms, and boiler services all happen on a predictable schedule. The mistake is not saving for them in advance.

A sinking fund is a small pot you contribute to monthly so that when the expense arrives, the money is already there. It does not come out of your emergency fund and it does not go on a credit card.

| Sinking fund | Estimated annual cost | Monthly contribution needed |

|---|---|---|

| Car MOT and servicing | £300–£500 | £25–£42 |

| Christmas and birthdays | £400–£800 | £33–£67 |

| Annual insurance (home, car) | £400–£800 | £33–£67 |

| Home maintenance | £200–£500 | £17–£42 |

| Holidays | £500–£1,500 | £42–£125 |

Start with whichever irregular expense has caught you out most in the past 12 months and build from there.

Step 6 — Make progress visible

Consistency is much easier to maintain when you can see it working. Name your savings pots with specific goals rather than leaving them as a generic savings account. "Emergency fund — £1,200 of £4,500" is far more motivating than "Savings — £1,200."

Review your savings once a month — not daily. Daily checking tends to create anxiety rather than motivation. A monthly review lets you celebrate progress, adjust if needed, and stay connected to your goals without it becoming a source of stress.

Track milestones: the first £100, the first £500, the point where your emergency fund covers one month of expenses. Small wins matter more psychologically than people expect.

What to do when saving feels impossible

If there genuinely is nothing left at the end of the month, the problem is either income, expenses, or both — and fixing it starts with understanding which. A month of honest tracking usually reveals at least one or two areas where spending is higher than expected.

If expenses are genuinely at the minimum, even saving £10 or £20 a month has value. It builds the habit, creates a small buffer, and puts you in a position to increase the amount when circumstances change. Starting small is not failure — not starting at all is.

For more ideas on reducing outgoings without feeling deprived, see our guide to 50 easy ways to save £100 a month. If debt repayments are making it hard to save, our guide to debt consolidation options in the UK covers ways to reduce monthly outgoings.

Frequently asked questions

- How much should I save each month in the UK? There is no universal answer — it depends on your income and expenses. As a starting point, aim for 10% of take-home pay. If that is not possible, start with whatever you can automate and increase it over time.

- Is it better to save or pay off debt? Build a small emergency fund of £500–£1,000 first, then focus on clearing high-interest debt (credit cards, overdrafts). Once high-interest debt is cleared, increase your savings rate. See our emergency fund guide for a detailed breakdown of this approach.

- What is the best savings account for consistent saving in the UK? An easy-access savings account paying competitive interest is the best starting point. See our guide to best high-interest savings accounts in the UK for current options.

- Does the 50/30/20 rule work in the UK? As a rough framework, yes — but it needs adapting for UK housing costs. Protecting the savings portion (even at 5–10%) is more important than hitting the exact percentages.

- What if I have an irregular income? Save a percentage of each payment rather than a fixed amount. When income is higher, save more. When it is lower, save less. The consistency of the habit matters more than the consistency of the amount.