Best Low-Risk Investments UK for Beginners (2026 Guide)

Visual summary of key points from 'Best Low-Risk Investments UK for Beginners (2026 Guide)'

Essential UK Budgeting & Personal Finance Guides for 2026

Discover practical tips, tools, and strategies to manage your money, save effectively, and stay on top of your finances.

Check out our key articles: How to Create a Simple Budget, How to Save £500 in 3 Months, Understanding Credit Scores in the UK.

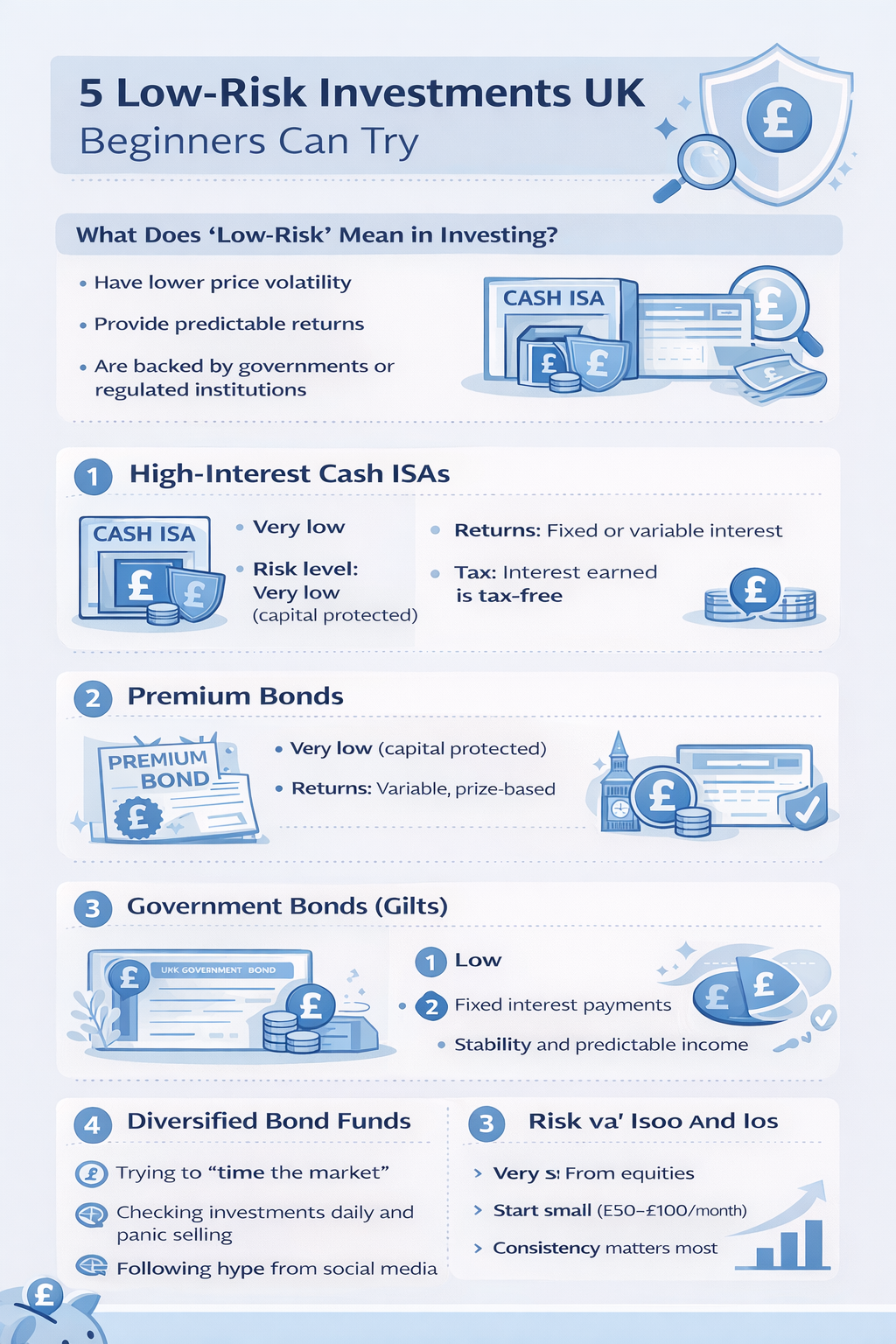

5 Low-Risk Investments UK Beginners Can Try in 2026

Not every investor wants to ride the volatility of the stock market. If you are new to investing, risk-averse, or investing money you might need within a few years, lower-risk options make more sense than diving straight into equities.

This guide covers five genuine low-risk investment options available to UK beginners in 2026 — with current rates, practical access details, and honest assessments of where each one fits. All options are either government-backed or FCA-regulated.

Important: Even low-risk investments carry some level of risk. This article is for informational purposes only and does not constitute regulated financial advice. Capital is at risk.

What low-risk actually means in investing

Low-risk in investing typically means one or more of the following:

- Capital protection — your original deposit is unlikely to fall in value

- Low volatility — the value does not swing dramatically day to day

- Predictable returns — you know roughly what you will earn in advance

- Government or institutional backing — a regulator or government guarantees some or all of your money

The trade-off is returns. Genuinely low-risk options typically produce lower long-term returns than equities. The question is always: does the lower return justify the lower risk for your specific goal and time horizon?

Quick comparison

| Option | Risk level | Typical return (2026) | Capital protected? | Best time horizon |

|---|---|---|---|---|

| Cash ISA (easy access) | Very low | 4.0–4.8% | Yes (FSCS up to £85k) | Any — including short term |

| Premium Bonds | Very low | Equivalent ~4.4% prize rate | Yes (government-backed) | Any — no lock-in |

| UK government bonds (gilts) | Low | 4.0–4.5% yield | Yes if held to maturity | 1–10+ years |

| Diversified bond funds | Low–medium | 3.5–5.5% (variable) | No — value can fall | 3–7 years |

| Global index funds | Medium | Historically 6–8% long term | No — value can fall | 5+ years minimum |

1. Cash ISA (easy access)

A Cash ISA is a tax-free savings account — not technically an investment, but the safest way to grow money without any market exposure. Interest earned inside a Cash ISA is completely free from income tax, making it more efficient than a standard savings account for higher-rate taxpayers or anyone who has used their £1,000 Personal Savings Allowance.

In 2026, competitive easy-access Cash ISA rates from providers including Trading 212, Chip, and Plum are offering 4.0–4.8% AER — meaningfully higher than inflation. Your money is protected up to £85,000 per provider under the Financial Services Compensation Scheme (FSCS).

- Risk level: Very low — capital fully protected

- Current returns: 4.0–4.8% AER (easy access, March 2026)

- Annual allowance: Up to £20,000 (shared with other ISA types)

- Access: Instant or within a few working days depending on provider

- Best for: Short-term goals, emergency funds, anyone unwilling to accept any capital risk

The main limitation: Cash ISA returns rarely outpace inflation meaningfully over the long term. For goals five or more years away, the other options below are worth considering.

For current best rates, see our guide to best high-interest savings accounts in the UK.

2. Premium Bonds

Premium Bonds are issued by NS&I (National Savings and Investments), which is backed by the UK Treasury. Instead of paying interest, your bonds are entered into a monthly prize draw with prizes ranging from £25 to £1,000,000. Your original deposit is 100% safe — you can never lose the money you put in.

The current prize fund rate is equivalent to approximately 4.40% AER (as of March 2026), though this is an average — your actual return depends entirely on whether you win prizes. Statistically, smaller holdings (under £1,000) have a lower effective return than larger holdings due to the way prizes are distributed.

- Risk level: Very low — capital 100% protected by HM Treasury

- Effective prize rate: ~4.40% AER equivalent (March 2026)

- Minimum investment: £25

- Maximum holding: £50,000

- Access: Withdraw within a few working days

- Tax: All prizes are tax-free

- Best for: Cautious savers, anyone wanting government-backed security with a chance of larger prizes

Premium Bonds are not guaranteed to beat a Cash ISA — some months you may win nothing. But with capital fully protected and no tax on prizes, they remain one of the most popular savings products in the UK. Buy directly at nsandi.com.

3. UK government bonds (gilts)

When you buy a UK government bond (gilt), you are lending money to the UK government in exchange for regular fixed interest payments (called the coupon) and the return of your full investment at the end of the term (called maturity). As long as you hold the gilt to maturity, you know exactly what you will earn.

Gilt yields in 2026 are at levels not seen for over a decade. Two-year gilts are currently yielding around 4.0–4.2%, while 10-year gilts yield approximately 4.3–4.5%. These are competitive with Cash ISAs but with the added benefit of locking in a fixed rate for a defined period.

- Risk level: Low — UK government default risk is negligible; price risk exists if sold before maturity

- Current yields: 4.0–4.5% depending on term (March 2026)

- Access: Via a Stocks and Shares ISA or GIA on most investment platforms; or directly via the UK Debt Management Office

- Best for: Investors who want a fixed, predictable return for a defined period and are comfortable not selling early

One important caveat: gilt prices move inversely to interest rates. If you need to sell before maturity and interest rates have risen, your gilt may be worth less than you paid. Hold to maturity to guarantee your return.

4. Diversified bond funds

Rather than buying individual gilts, a bond fund pools money from many investors to hold a diversified portfolio of government and corporate bonds. This removes the need to select individual bonds and provides automatic diversification across different issuers, maturities, and geographies.

Bond funds do not have a fixed maturity date — the value fluctuates daily with interest rate movements and credit conditions. They carry more risk than individual gilts held to maturity but less volatility than equity funds.

- Risk level: Low to medium — value can fall, particularly when interest rates rise

- Typical returns: 3.5–5.5% annually over the medium term (not guaranteed)

- Examples: Vanguard UK Government Bond Index Fund, iShares Core UK Gilts ETF (IGLT), Vanguard Global Bond Index Fund

- Ongoing charges: Typically 0.07–0.20% per year

- Access: Via any major UK investment platform inside an ISA

- Best for: Investors with a 3–7 year horizon who want lower volatility than equities but better long-term returns than cash

Bond funds are often used alongside equity funds to reduce overall portfolio volatility — a classic "60/40" portfolio holds 60% equities and 40% bonds. For a beginner building their first portfolio, a bond fund is a sensible component rather than a standalone investment.

5. Global index funds (low-cost, diversified)

A globally diversified index fund is not low-risk in the same sense as a Cash ISA or Premium Bond — the value will fall during market downturns, sometimes significantly. However, compared to picking individual UK stocks or sector-specific funds, a global index fund is the lowest-risk way to invest in equities because it spreads your money across thousands of companies worldwide.

The long-term case is compelling: a globally diversified index fund invested for 10 or more years has historically produced positive real returns in every major market. The risk is primarily time risk — needing to sell during a downturn before the market has recovered.

- Risk level: Medium — value can fall significantly in the short term

- Historical long-term returns: 6–8% annually on average (not guaranteed)

- Examples: Vanguard FTSE All-World ETF (VWRL), iShares Core MSCI World ETF (SWDA), Vanguard LifeStrategy 60% Equity Fund

- Ongoing charges: 0.10–0.25% per year

- Best for: Investors with a minimum 5-year horizon who can tolerate short-term fluctuations in exchange for higher long-term growth

- Not suitable for: Money you might need within five years

For a full guide to getting started with index funds and choosing a platform, see our investing for beginners UK guide.

How to choose the right option for you

The right low-risk investment depends entirely on your time horizon and what you need the money for:

| Goal | Time horizon | Recommended option |

|---|---|---|

| Emergency fund | Immediate access needed | Easy-access Cash ISA or Premium Bonds |

| Saving for a house deposit | 1–3 years | Cash ISA (fixed term for better rate) or Premium Bonds |

| Medium-term goal (holiday, car, home improvement) | 2–5 years | Cash ISA, gilts, or cautious bond fund |

| Retirement or long-term wealth | 10+ years | Global index fund inside ISA or SIPP |

If you are unsure where your finances stand before investing, our guide to saving consistently on a UK budget covers the foundations to have in place first.

Frequently asked questions

- What is the safest investment in the UK? Premium Bonds and Cash ISAs with FSCS-protected providers are the safest options — both protect your original capital fully. Premium Bonds are backed directly by HM Treasury with no upper protection limit.

- Can I lose money in a bond fund? Yes. Bond fund values fall when interest rates rise. Unlike individual bonds held to maturity, bond funds do not have a fixed return. They are lower risk than equity funds but not capital-protected.

- Are Premium Bonds worth it in 2026? At an equivalent prize rate of around 4.40%, Premium Bonds are competitive with easy-access Cash ISAs. The advantage is that all prizes are tax-free and capital is fully protected. The disadvantage is that returns are random — you may win more or less than the average rate in any given year.

- What is the minimum amount to start investing in low-risk options? Premium Bonds require a minimum of £25. Cash ISAs can often be opened with £1. Government bonds and bond funds are accessible through most UK investment platforms with no minimum beyond the platform's own requirements.

- Is a Cash ISA better than a savings account? For most people, yes — interest inside a Cash ISA is completely tax-free, whereas savings account interest is only tax-free up to your Personal Savings Allowance (£1,000 for basic rate taxpayers, £500 for higher rate). Once you exceed that allowance, a Cash ISA is clearly better.